With rising housing costs across the country, the federal government has been pressured to do something to help younger first-time home buyers who have been priced out of the higher priced areas such as Toronto and Vancouver. The federal budget for 2019 has been released and there are two main additions regarding real estate and first-time home buyers.

CMHC First-Time Home Buyer Incentive

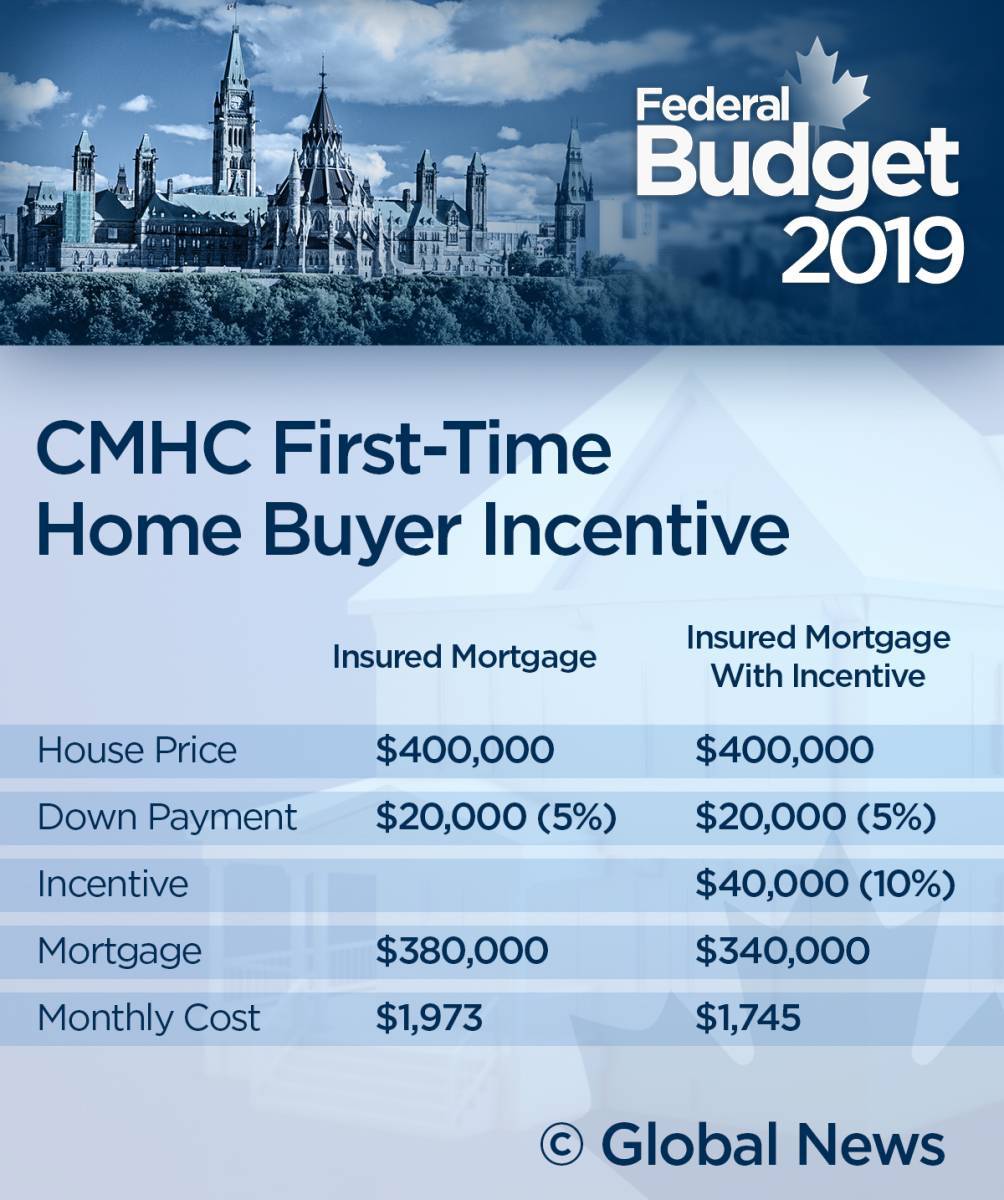

The budget introduced the Canadian Mortgage and Housing Corporation (CMHC) First-Time Home Buyer Incentive. This allows prospective buyers who have the minimum down payment for a home to apply to finance between 5% and 10% of their mortgage via a shared equity program. Buyers can get up to 10% on newly constructed homes while 5% applies to existing homes. This would lower the mortgage amount borrowed and would help first-time home buyers qualify for a higher mortgage, even with the mortgage stress test, while also lowering their monthly mortgage payments.

This incentive would only apply to insured mortgages and the buyer would still have to come up with the minimum 5% down payment. Applicants must have a maximum household income of no more than $120,000 and the purchase price of the home can only be 4 times their household income. So, for a family of first-time home buyers with an annual household income of $80,000 the total mortgage size would be $320,000.

The budget document states “For example, if a borrower purchases a new $400,000 home with a 5% down payment and a 10% CMHC shared equity mortgage ($40,000), the borrower’s total mortgage size would be reduced from $380,000 to $340,000, reducing the borrower’s monthly mortgage costs by as much as $228 per month.”

Buyers will still have to repay the loan, although it is unclear at this point what the terms would be. Applicants still must qualify under the federal stress test, which ensures that borrowers will be able to keep up with their payments if their interest rates were to increase. However, the lower mortgage means the borrower would only need to qualify for the lower mortgage amount.

The finance department is hoping the new program will pass in time for a September, 2019 launch.

Home Buyers’ Plan (HBP) Gets An Increase

The amount a borrower can withdraw from their RRSP for a down payment using the Home Buyers’ Plan (HBP) has been increased for the first time in 10 years. With increasing home values the federal government has increased the amount you can withdraw from your RRSP account from $25,000 to $35,000, or $70,000 per couple. The new limit will apply to withdrawals made after March 19, 2019, making it effective immediately.